The past year was clearly more profitable for the chicken industry, though no less challenging than 2020. Trends that emerged during the past year will have implications for the next 52 weeks. Factors that influenced production and profitability included both extrinsic and intrinsic concerns:-

| |

COVID and Labor COVID and Labor |

| |

|

The infection dominated the national economy and disrupted markets. Shifts in demand for products resulted in changes in presentation with some integrators displaying a considerable level of flexibility and adaptation representing a competitive advantage. With the availability and extensive administration of effective vaccines the immediate and critical problems associated with availability of labor are now less pressing. Suppression of COVID will continue at a high cost both from increased wages and benefits but also in expenditure on preventive measures. The industry will now be obliged to introduce mechanization and robotics to displace manual and repetitive labor. Fortunately technology has advanced to permit purchase and installation of off-the-shelf lines to displace labor in first processing, portioning and deboning, albeit requiring capital expenditure. |

| |

Inflation |

| |

|

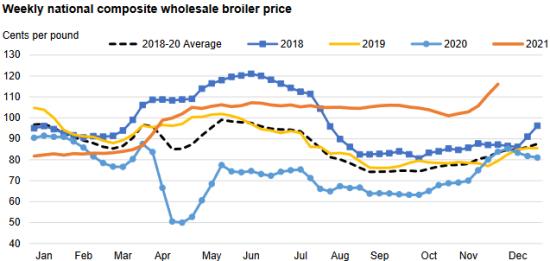

The past year witnessed high inflation in all inputs. Increased cost of feed ingredients, fuel, labor and packaging detracted from gross profit. The upward trend will continue in 2022 given the difficulty for the Federal Reserve to suppress inflation by increasing interest rates without precipitating a recession. Management of cash-flow, hedging and financial planning will be important concerns in 2022. |

|

| |

Regulatory Environment |

| |

|

The current Administration has adopted policies opposing large-scale processing of red meat and poultry, failing to recognize efficiencies of scale and at the same time promoting infeasible alternatives with public funds. The intercession of the Department of Justice in the proposed acquisition of Sanderson Farms is but one of a number of actions regarded as opposing a well-functioning industry, benefitting contractors, consumers and shareholders. Increased regulatory action will be evident in 2022 in the areas of labor, the environmental and trade. |

| |

Production Efficiency |

| |

|

2021 was marked by relative freedom from disease. Flock livability has held at 95 percent and post-mortem condemnation at 0.5 percent of processed mass. There is however a growing risk of H5N1 avian influenza that will require considerable upgrading of structural biosecurity and diligence in operational biosecurity. |

|

| |

Consumerism and Welfare |

| |

|

Despite an undertone of concern over shelf prices most consumers recognize that inroads into budgets are due to inflation without a sense of price gouging. Given the price of alternative proteins, chicken is regarded as an available, relatively low-priced nutritious food. Demand should increase in 2022 over the current year at the expense of red meat. Plant based alternatives to chicken will not represent any meaningful competition in either retail or food service segments in 2022. Welfare along with sustainability will continue to be issues of concern in the coming year. Higher levels of welfare including less efficient “slow growing” strains or “free-range” products will be marketed at high prices to a small but affluent concerned demographic without materially affecting existing metrics in the industry. |

| |

Sustainability |

| |

|

Major chains will impose increasingly higher standards of sustainability involving conservation of energy, packaging, use of water and greenhouse gas emissions. Defining the components in the supply chain extending from contractor to end user that will be required to make investments and how costs will be passed on are questions to be addressed more intensively in 2022. |

| |

Exports |

| |

|

Exports to China were disappointing in 2020 with the exception of feet. There are no potential prospects for any incremental demand from that nation given the restoration of the hog herd and overproduction of white-feathered broilers. Rabobank note a moderate increase in international trade but the U.S. offers predominantly leg quarters, comprising the major export product that as a commodity offers little prospect of added value or pricing power. |

| |

Production |

| |

|

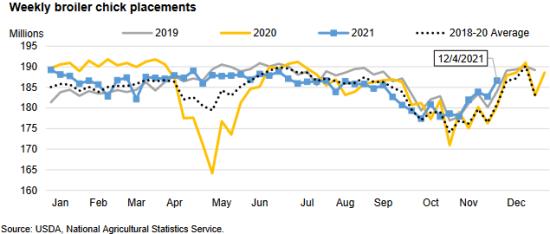

USDA projects a 1.7 percent increase in output in 2022 to 45,600 million lbs. with an almost corresponding 1.6 percent increase in consumption. This should be attainable given increasing hatchability and a compensatory increase in placements of heavy-strain parents following the self-inflicted problem of inappropriate selection. |

There will be many challenges facing the chicken industry in 2022. Let us work for a reduction in COVID by increasing rates of vaccination, preventing avian influenza through exclusion and biosecurity and restraining the socialistic inclinations of the Administration.